Personal Financial Planning Made Simple

You may feel unbalanced and confused in today’s world if you don’t have well thought out strategies for managing your finances. Personal financial planning is the solution to it. It is not only saving money that is needed – It is the creation of a life where finances go hand in hand with fulfilling goals. This is the main motto at NHI Money – Everyone, regardless of their income, deserves accessible and tailored professional financial services.

From one end to the other, this guide will prepare you to make confident decisions by detailed steps of personal financial planning which includes: budgeting, saving, and investing, so that you can make knowledgeable and deliberate decisions. Starting out, or even refining your approach – All needs are catered to with the below steps aimed at helping you achieve wealth that lasts a lifetime.

Why Personal Financial Planning Matters

Personal financial planning is not just for the wealthiest, it is an integral part of any individual’s life competency scheme. Lack of a plan exposes you to price fluctuations, job changes, and sudden expenses. Having a strategic plan empowers your finances and helps you in preparing for the unexpected.

A personal finance study conducted by the National Financial Educators Council in 2023 highlighted that 72% of Americans felt more confident about their overall financial well-being after formulating a personal plan.

At its core, personal financial planning empowers you to:

- Track your income and expenses with purpose

- Eliminate debt without sacrificing lifestyle

- Save for emergencies and long-term goals

- Invest strategically based on your timeline and risk tolerance

- Enjoy retirement without financial fear

Key Components of a Strong Personal Financial Plan

Before we jump into the details, let’s discuss what makes a financial plan efficient in the first place. These principles guide every successful plan:

- Budget Planning & Control: Manage spending by creating personalized monthly budgets that align with your priorities.

- Expenses, Debt, and Payment Management: Plan how to repay your high interest debt while minimizing future debt exposure.

- Saving for the Future & Emergency Fund Allocation: Guarantee your continuity in the face of unforeseen circumstances.

- Investing for Positive Returns: Increase your wealth by acquiring financially marketable assets such as stocks and bonds.

- Retirement & Future Planning: Set goals for long-term security and peace of mind after you stop working.

Each of these areas works together, and skipping one can compromise the rest. Let’s explore each in depth.

Creating a Personal Budget That Works for You

A personal budget is the heartbeat of any strong financial plan. Done right, it keeps your goals in view and your money working efficiently. The key is to design a system that adapts to your lifestyle and evolves as your needs change.

The 50/30/20 Rule

This popular rule breaks your income into three simple categories:

| Category | % of Income | Purpose |

| Needs | 50% | Housing, utilities, groceries, bills |

| Wants | 30% | Dining out, hobbies, travel |

| Savings/Debt Repayment | 20% | Emergency fund, investments, loans |

This method is beginner-friendly, flexible, and easy to apply to monthly budgeting. It gives structure while allowing some freedom. In personal financial planning, this rule helps build discipline without making you feel restricted.

Tracking Expenses

Analyzing your spending behavior is of utmost importance. Remember; you can’t improve what you haven’t measured. Constant review of your spending helps eliminate waste, identify patterns, and alter spending.

Pro tip: Use the Song Nhi App to easily categorize and track daily spending. It offers smart insights, automated syncing with bank accounts, and visual reports that help you stay aligned with your personal financial planning goals.

| Tool | Benefit |

| Song Nhi App | Real-time tracking, insights, reminders |

| Spreadsheet | Fully customizable |

| Bank alerts | Helps monitor overspending |

The right tools make budgeting feel effortless – not overwhelming.

Adjusting for Life Changes

Life changes, and your budget should too. Promotions, job loss, moving cities, having a child, or health issues – these all affect your income and expenses. Regularly revisiting your budget keeps it relevant.

Update your budget every 3–6 months or after major changes. Use it to reevaluate priorities and redirect funds. This flexibility is a cornerstone of successful personal financial planning, especially when your financial goals evolve over time.

Cutting Unnecessary Expenses

Budgeting doesn’t mean eliminating joy – it means spending intentionally. Review your expenses and ask:

- Do I really use this subscription?

- Can I cook more at home?

- Are there cheaper alternatives?

Small savings add up. Canceling a $10/month service saves $120/year. Replacing takeout with home meals could save hundreds. Reinvest these savings into your emergency fund or investments – an essential habit in long-term personal financial planning.

| Expense Category | Potential Cut | Annual Savings |

| Streaming | Cancel extras | $120–$180 |

| Dining Out | 1 less meal/week | $800–$1,200 |

| Gym | Switch to home | $300–$600 |

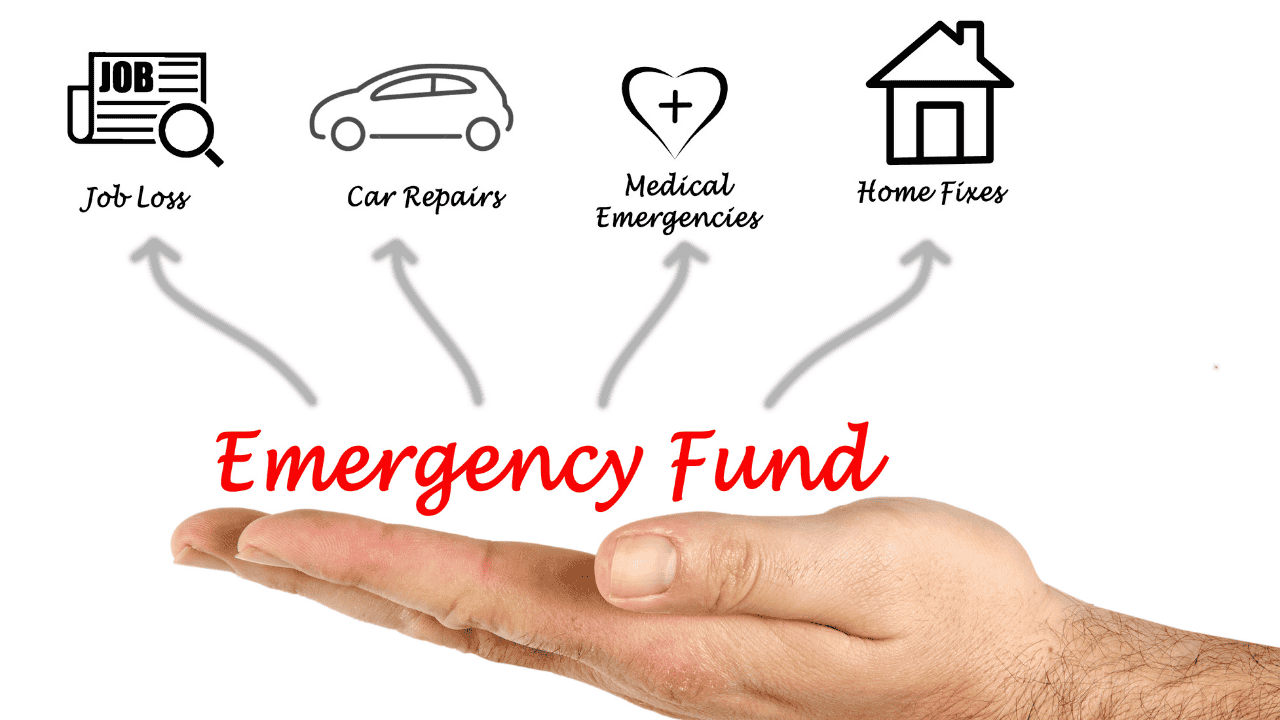

How to Build an Emergency Fund

An emergency fund is your financial shock absorber. Whether it’s a job loss, medical bill, or unexpected car repair, this fund protects you from going into debt during tough times. It is one of the most fundamental steps in personal financial planning, yet many overlook it until it’s too late.

Building an emergency fund is not about saving a huge sum overnight, it’s about creating a consistent habit that strengthens your financial resilience over time. Let’s break it down step by step across the four essential areas below:

Why Do You Need an Emergency Fund?

Life is unpredictable. Emergencies happen when you least expect them – and often at the worst time.

Without an emergency fund, people tend to rely on:

- Credit cards, leading to high-interest debt

- Personal loans, which can be hard to pay off

- Or borrowing from family, which strains relationships

A well-funded emergency reserve ensures that your daily life isn’t derailed by short-term crises. It gives you peace of mind – a priceless asset in personal financial planning. You’ll be able to handle emergencies with confidence instead of panic.

How Much to Save

A good rule of thumb is 3–6 months of living expenses. If your job is unstable or you’re self-employed, aim closer to 6–9 months.

| Household Type | Minimum Savings Goal |

| Single with stable income | 3 months expenses |

| Dual-income household | 3–6 months expenses |

| Self-employed/freelancer | 6–9 months expenses |

Start small. Even $500 – $1,000 can cover minor emergencies. Once you reach that, gradually build up toward the full amount. Remember: It’s okay if it takes months or even a year – to build it. The key in personal financial planning is progress, not perfection.

Best Places to Keep Emergency Savings

Keep these funds liquid and accessible, but separate from everyday accounts to reduce temptation.

| Option | Pros | Cons |

| High-yield savings | Earns interest, FDIC insured | Limited transactions/month |

| Money market accounts | Slightly higher rates, safe | May require a higher balance |

| Online banks | Easy access, no fees | Withdrawals take 1–2 days |

Avoid tying this money up in stocks or long-term CDs – this isn’t investment capital.

Saving on Autopilot

The easiest way to build an emergency fund? Automate your savings.

- Set up a weekly or bi-weekly transfer from checking to your savings

- Use round-up apps that save spare change from purchases

- Allocate part of every bonus, tax refund, or freelance income

Automation removes willpower from the equation. You’ll be surprised how fast it grows when you don’t have to think about it. As part of your broader personal financial planning strategy, automating savings gives structure to your goals and reduces decision fatigue.

Debt Management: Strategies to Pay Off Debt Faster

As you know, debt can quietly drain your income and delay financial freedom. Managing it well is key to successful personal financial planning. Below are proven strategies to pay down debt quickly and build better credit.

Snowball vs. Avalanche Method

Choosing between the snowball and avalanche methods is a key decision in personal financial planning.

- Snowball Method: Focus on paying the least amount first. This will help build motivation and momentum, which is really helpful if you are new to the world of debt management.

- Avalanche Method: Prioritize paying debts with the highest interest rates. It will save you more money in the long run, but you may not feel progress as quickly.

| Method | Strategy | Best For |

| Snowball | Pay smallest debt first | Motivation, quick wins |

| Avalanche | Pay highest interest first | Saving the most money long-term |

Each method works – the best choice depends on your mindset and long-term goals. Whichever path you choose, make it part of your broader personal financial planning strategy.

Consolidation and Refinancing

Managing multiple high-interest debts simultaneously can be stressful, but debt consolidation or refinancing can provide some financial relief.

- Debt consolidation brings together several debts, such as credit cards or personal loans, and transforms them into one new loan with a lesser interest rate or extended repayment period. This provides ease in managing payments and could reduce total interest payout over time.

- Refinancing works the same way, but instead of the loan being replaced with a new one, an existing loan (usually a mortgage, student loan or auto loan) is exchanged for a new one with better terms.

Both strategies can improve available cash flow every month for flexible financial planning. But remember: consolidation is only effective if you manage to control accruing new debt after the process. It is a tool, not a solution.

Avoiding Bad Debt

Not all debt is equal. A good debt such as a mortgage or a student loan can help the borrower build wealth or increase income in the future. But bad debt drains your finances without long-term value.

Bad debt typically includes:

- High-interest credit cards

- Buy-now-pay-later schemes

- Payday loans

- Loans for depreciating items (like luxury goods or gadgets)

Not falling into bad debt means you have to be honest with yourself when spending. It also means you know when trouble can start and how to stop them from snowballing into larger troubles. Personal financial planning separates what one might want now from what one truly needs in the future.

Rule of thumb: If it doesn’t increase your income or value as time goes on, then think twice before borrowing to fund it.

Boosting Your Credit Score

Your credit score affects most aspects of your financial life. This includes loan approvals, insurance, and rental applications.

To raise or maintain a healthy score:

- Pay on time, every time

- Keep credit utilization below 30%

- Don’t close old accounts unless necessary

Every component of your personal financial planning endeavor gets enhanced with a higher score. Lower interest rates on loans, better terms on loans, and ultimately greater flexibility and control are granted with higher scores.

You might also read:

Investing: How to Grow Your Wealth

We all know that protecting money is essential. But, over time, investing and helping your money grow is what builds wealth and wealth. At this stage of a financial planner’s work, your money starts working for you. You’re able to beat inflation and generate passive income, ultimately leading to a much more stable future.

One of the greatest benefits of compound interest is when it’s started early, and in the section below, we explore the fundamentals of investing so you can grow your financial security confidently.

Investment Basics

Investing refers to the process through which finances earmarked for consumption at a future date will be invested into different classes of assets such as stocks, bonds, real estate, etc. for the purpose of creating profits over a duration of time. There is risk involved during the investment period; however, there is also potential to reap much higher rewards compared to simply saving money.

Here are a few common types of investments:

| Asset Type | Description | Risk Level |

| Stocks | Ownership in a company | Medium–High |

| Bonds | Loans to government or companies | Low–Medium |

| Mutual Funds | Diversified portfolios | Medium |

| ETFs | Traded like stocks, diversified | Medium |

Understanding these basics is a crucial step in your personal financial planning strategy.

Risk vs. Reward

All kinds of investments include an element of risk – greater the potential reward, greater the risk. In personal financial planning, having a clear understanding of one’s risk tolerance is key for determining the correct investment options.

- Low Risk: Government bonds, savings accounts

- Medium Risk: Dividend-paying stocks, mutual funds

- High Risk: Cryptocurrencies, individual stocks

Strategically distributing investment across a range of different asset types helps ensure risk mitigation. This strategy aids in protecting an investor against substantial losses during market drops whilst allowing investment growth over time.

Long-Term vs. Short-Term Investing

Your financial goals determine whether you should invest short-term or long-term:

- Short-term: A house, wedding or vacation

- Long-term: Planning for retirement, children’s education, or simply for building wealth

Investors focusing on short-term goals may consider keeping their money in stable investment vehicles such as high interest savings accounts and money market funds. On the other hand, long-term investors willing to endure market volatility will be able to take advantage of compound returns. Solid long-term personal financial planning includes market exposure.

Retirement Accounts

Start with tax-advantaged accounts:

| Account Type | Tax Benefit | Notes |

| 401(k) | Pre-tax; employer matching | Maximize match contributions |

| IRA | Pre-tax or Roth options | Great for self-employed |

| Roth IRA | Tax-free withdrawals later | Ideal if you expect higher taxes in retirement |

Invest regularly, even if the amount is small. Time in the market beats timing the market.

Real Estate and Alternative Investments

Real estate can provide passive income and tax benefits. Other alternatives – like REITs, peer lending, or even collectibles – can diversify your portfolio.

But always do your due diligence. These assets are less liquid and require more hands-on involvement.

Retirement Planning: How to Secure Your Future

In this term, retirement is not an elusive goal – but rather a financial target that requires a systematic approach to achieve. A sound strategy for retirement should be one of the cornerstones of personal financial planning so you are able to enjoy your later years in life. Key concepts to consider when thinking about retirement planning will be explored next.

When Should You Start Saving?

Starting in your 20s or 30s gives your money more time to grow through compound interest. Even small monthly contributions can build a strong foundation over decades. For those starting later, it’s never too late – what matters is consistency and increasing your contributions over time.

Best Retirement Accounts

Choosing the right account can maximize your savings. Common options include:

| Account Type | Tax Advantage | Best For |

| 401(k) | Pre-tax contributions, employer match | Employees with benefits |

| IRA | Tax-deferred or tax-free growth (Roth) | Individual savers |

| RRSP (Canada) | Tax-deductible contributions | Canadian residents |

Having these accounts integrated into your personal financial strategies will ensure that investment growth is maximized while tax implications are kept to a minimum.

How Much Money Do You Need to Retire?

A rough estimate to aim for would be 70-80% of your income before retirement on an annual basis. Leveraging retirement planning calculators or working through the numbers with a financial planner can provide insight into your “retirement number” depending on the lifestyle you wish to lead, expenses, healthcare requirements, and where you plan to live.

Example:

| Annual Expenses | Estimated Amount Needed at Retirement (25 years) |

| $40,000/year | $1 million |

| $60,000/year | $1.5 million |

Remember, the more detailed your plan, the smoother your path to retirement.

Social Security and Passive Income

Although Social Security may serve as the basic income earmarked for you, it shouldn’t be your sole focus. It is always best to also plan for supplemental passive income channels like rental properties, dividends, and annuities. Integrating these aspects into your personal financial planning will provide you with a sense of tranquility and bolster your financial well being.

Pro tip: It is imperative to have multiple streams of retirement income, this minimizes reliance on one stream or one area for income during retirement which decreases risk and enhances flexibility.

Financial Planning for Different Life Stages

Your evolving life and age will determine the personal financial planning requirements that need to be met. Each stage is accompanied by distinct risks, priorities, and advantages. Tailoring your plan accordingly helps you stay in control.

- 20s & 30s: Focus on building an emergency fund, paying off debt, and starting to invest early – time is your greatest asset.

- 40s & 50s: Increase retirement contributions, protect your income with insurance, and prepare for larger expenses like college or mortgages.

- 60s & Above: Focus on formulating set strategies and plans for withdrawal phase of retirement while factoring in legacy and healthcare considerations.

- Life Events: These new milestones like shifting careers, getting married, having kids, or even coming into an inheritance necessitate a change in your financial plan.

Further reading: